GST in India for gold

GST in India brought on 1st July 2017. It has begun new era in taxation in India. GST in India for gold in different structures has examined finally in this blog. GST subsumed VAT, service tax, excise duty and a few other indirect charges charged on domestic transactions. Tax on the making charges on gold jewellery had presented under GST. Then basic custom duty keeps on getting collection on the import of gold from different nations and the duty of IGST.

What is GST on gold?

Gold bars or gold jewellery fall within the meaning of ‘Goods’ according to the GST regulation. Under Section 7 of the CGST Act, the supply of gold (with no work) has a view as the supply of goods. GST for gold is as per the following-

GST rates on gold buy and GST on gold making

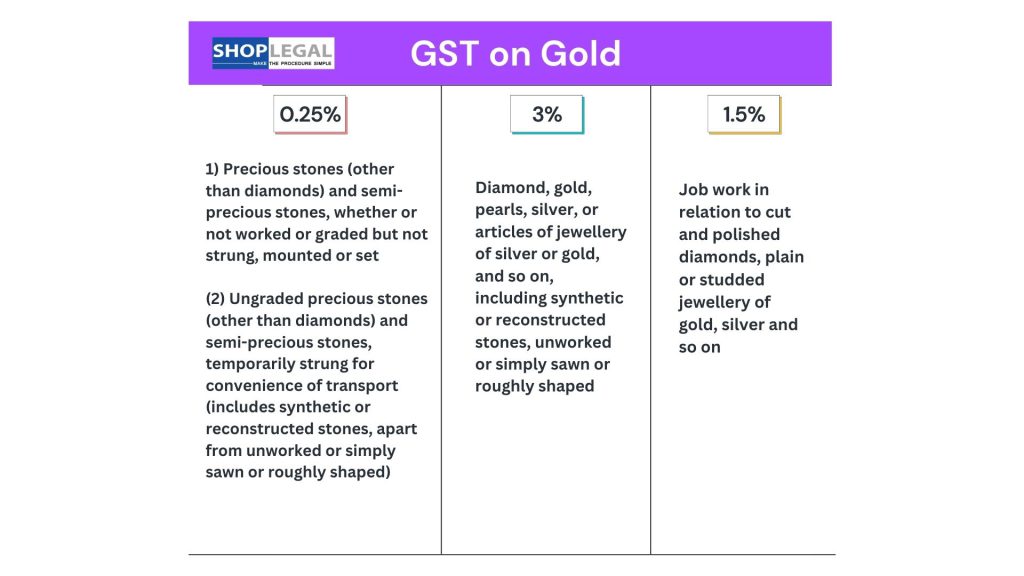

According to Section 8 of the CGST Act, selling gold ornaments or jewellery to the everyday person is a composite supply of service and goods. The gold utilized has viewed as goods and making charges or value addition is towards work.

Since the principal supply is the sale of gold, the GST rate of 3% will has imposition rather than 5% on the total value of jewellery; whether making charges shown independently. The CBIC has explained this in its sectoral FAQs on what is the GST on gold, remembering GST for gold rate.

The GST registered by GST registration in Coimbatore has threshold limits that generally apply to typical citizens apply to organizations in gold mining and distribution also. Further, the composition scheme under section 10 of the CGST Act is accessible to organizations selling gold.

Numerous gold traders or venders or diamond setters take the services of goldsmiths and experts who do work on the gold bars or gold rolls provided by them to make ornaments. It has viewed as a supply of service. The goldsmiths will tax for their service known as making charges which will draw in GST of 5%.

In the event that these goldsmiths or experts are not enlisted under GST by GST registration in Chennai, the gold shipper or diamond setter should pay GST at 5% on a converse tax premise.

Purchasers who approach the goldsmiths without anyone else will likewise need to pay 5% GST assuming that the goldsmith has enrollment under GST.

GST that may have registration by GST registration in Bangalore isn’t charged in the event that unregistered people sale gold jewellery or trade gold ornaments to purchase new ones at ornaments shops. It has no viewed as advancement of business and is out of the extent of supply under GST.

Nonetheless, if vendors or gold organizations like Attica Gold organization, Aashraya Gold Organization or Manappuram Gold Advance, and so on buy and sell recycled gold jewellery, GST applies on the value of such gold determined according to the rule 32(5) of CGST Rules, subsequent to fulfilling the circumstances.

Fix deals with ornaments will have the view as the making charges for which GST has charged independently at 5%.

GST Calculation on Gold

To set the specific situation, while working out GST on gold jewellery , GST on gold ornaments, GST on gold coin, GST on gold bar, GST on gold bar or GST on gold buy, cost incorporates the expense of separating and handling the gold, and the net revenue, yet does exclude making charges.

Nonetheless, the cost of gold jewellery furthermore includes making charges. Up to 30th June 2017, charges, for example, VAT and service tax were exacted on its cost. From that point, it had supplant by GST. The GST may have registration under GST registration in Cochin.

Effect of GST on Gold

From the above examination between ‘before GST’ and ‘under GST, as a composite supply, we can see a cost ascent of some amount which is an inexact increment of 1.1% under GST.

The cost rise is because of the expanded expense rate from 2% to 3% under GST on unadulterated gold or gold bars.

Further, GST which is registered by GST registration in Trivandrum is recently required on the making charges, and it was prior not present in the past circuitous assessment system. These elements have added to the cost rise.

Budget 2019 additionally expanded the custom duty on gold bars imported from outside India. It is 12.5% against the previous rate of 10%.

GST on Gold Exemptions

A GST exemption had declaration at the 31st GST Council meeting on 22 December 2018. Likewise, GST has no charge for the supply of gold made by the advised organization to GST-enrolled gold ornaments exporters.

The move has limited the GST burden on Indian exporters of gold jewellery and most likely made Indian gold commodities more cutthroat on the world market.

Be that as it may, domestic purchasers of gold jewellery have no adverse impact. The GST can have registration by GST registration in Hyderabad.

e-Way bill rules for gold and its forms

Preceding 13th September 2022, CGST Rule 138(14) states that moving gold in any structure including jewellery, goldsmith’s goods and articles (Chapter 71), didn’t need an e-way bill. Consequently, whether the provider or beneficiary of gold is enrolled under GST registration in Madurai could move gold without conveying an e-way bill.

From thirteenth September 2022, according to particular state warnings, the NIC has empowered a different window for producing e-way charges for moving gold, gold jewellery or valuable stones.

Availability of input tax credits for GST on gold business

The jeweller or gold trader can claim Input Tax credit (ITC) paid on the unrefined substances utilized, i.e., gold and other work charges brought about. When the gold trader pays tax on a converse tax reason for supply from an unregistered work worker, he can claim the ITC on such expense.

Well known Advance Decisions on GST on gold under GST

- Karnataka AAR on account of M/s Attica Gold Pvt. Restricted all together KAR/ADRG/15/2020 dated 23rd Walk 2020

Matter/Issue:

The candidate gold organization sales spot cash for gold and deliveries the vowed gold at the ongoing business sector cost enrolled under GST registration in Salem.

On account of recycled acquisition of gold from unregistered people in the event that there is no adjustment of the sort/nature of the goods:

Ruling:

Valuation:

Whether the GST that had registration by GST registration in Erode is charged exclusively on the distinction between the selling cost and the price tag, as given in Rule 32(5) of the CGST Rules?

ITC Claim:

Whether the organization can claim ITC assuming buys have production using the vendor from whom the negligible plan is material?

Valuation:

If the organization lifts a receipt as recycled goods or arrangements in it with practically no adjustment of structure/kind of the ornaments bought, the valuation of the gold jewellery bought from unregistered people will be according to Rule 32(5) of the CGST Rules.

The valuation for GST that is registered through GST registration in Trichy is the contrast between the selling cost and the price tag on the off chance that it is positive. Be that as it may, if that the price tag is more than the selling value, no GST has imposition. Also, non-availment of the input tax break will be an extra condition.

ITC Claim:

In the event that the acquisition of recycled gold jewellery is from an enlisted individual, ITC is accessible. In this case, the threshold scheme, won’t be accessible for the gold organization on its further deal.

- Maharashtra AAR on account of M/s Biostadt India Restricted all together GST-ARA-72/2018-19/B-165 Mumbai dated twentieth December 2018

Matter/Issue:

The candidate organization is occupied with crop assurance synthetic substances and cross breed seeds. It sent off a deals impetus crusade – Kharif Gold Plan 2018. The plan sales 10 gm and 8 gm gold coins to its clients for buys over a specific amount and for making least payments, separately. The issue was as per the following:

ITC Claim:

Whether the input tax credit can have profit on the acquirement of gold coins utilized for directing deals advancement?

ITC Claim for comparative plans:

Whether ITC is accessible for some other comparative plans

Ruling:

ITC Claim:

No, ITC isn’t accessible for claims for bought gold coins. The distribution of gold coins isn’t the basic business of the citizen organization in consistence with Section 16 of the CGST Act.

Further, Section 17(5) on hindered ITC. It beats Section 16 prohibits ITC claims for removal of any bought goods as a present. The conveyance of gold coins under the plan is likewise has view as a ‘gift’.

ITC Claim for comparable plans:

No, ITC isn’t accessible for claims for some other comparable plans.

FAQ

The amount GST on digital gold?

GST on digital gold is 3% on all costs of insurance payment, cost of storage, and trustee fee, similar to the acquisition of physical gold. GST can be enrolled by GST registration in Karur.

Will individual case GST on gold?

A person who is selling gold ornaments and imports gold might pay IGST on it at 3%. He can claim GST on gold imported. In any case, people who are not in that frame of mind of gold can’t claim tax break. GST can have registration by GST registration in Tirupur.

Do we really want e-way bill for gold transportation?

Until the CBIC advises the evacuation of the exception in chapter 71 on gold, e-way bill need not have production. Nonetheless, NIC has refreshed the framework for a different window to produce an e-way bill for gold development.

About Us

We are SHOPLEGAL, the best service provider and we are serving our numerous clients over years.

Readers may scan the QR code below to share this blog.